Official Minnesota M1X Form in PDF

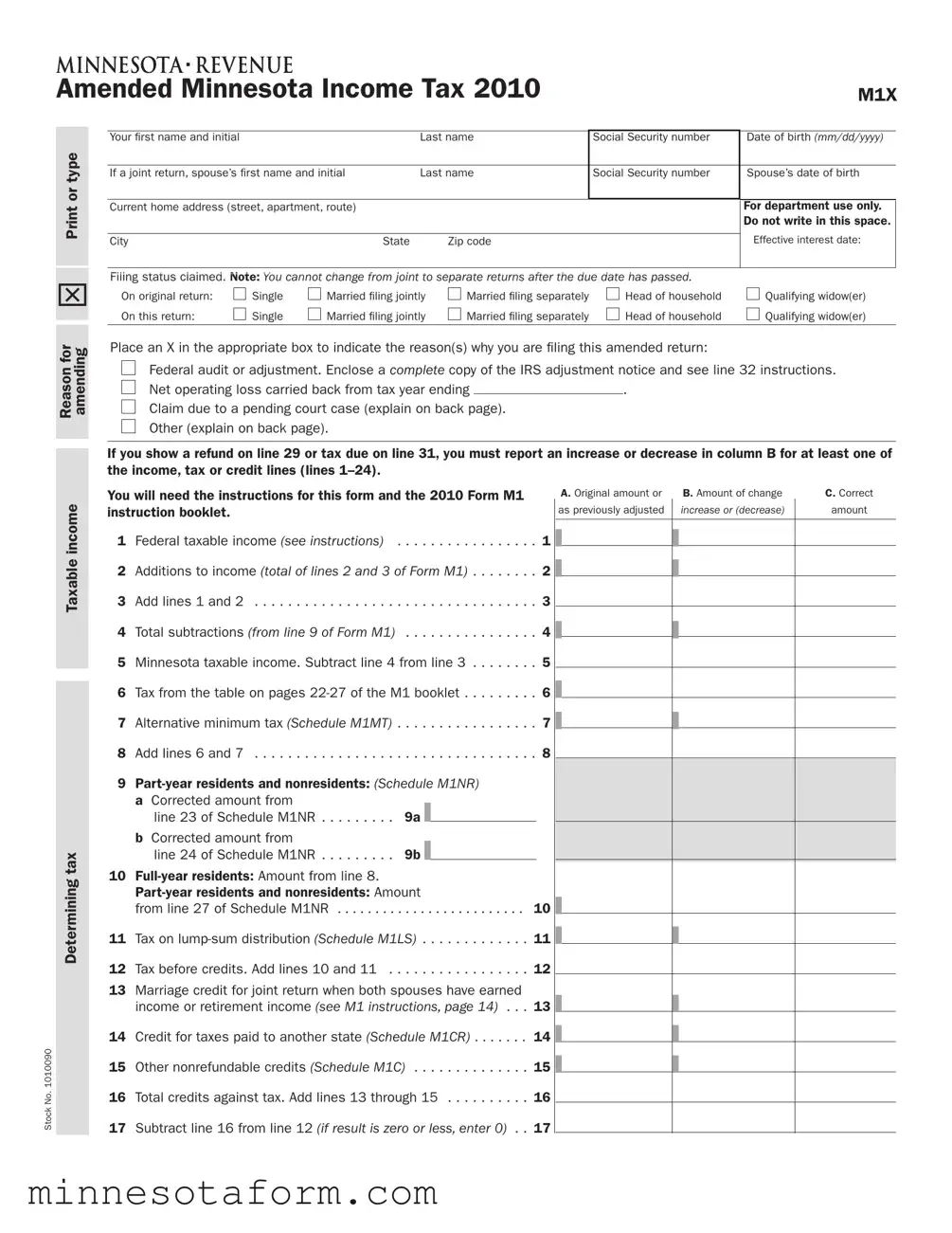

The Minnesota M1X form is an essential tool for individuals seeking to amend their 2010 Minnesota income tax return. This form allows taxpayers to correct errors or make changes to their original filing, ensuring that their tax obligations are accurately reflected. Key aspects of the M1X include the requirement to specify the reason for amending the return, such as adjustments due to a federal audit or changes in income. Taxpayers must provide personal information, including their Social Security number and filing status, which may be single, married filing jointly, or head of household. The form also requires detailed reporting of taxable income, additions, subtractions, and applicable credits. It is crucial to note that taxpayers cannot change their filing status from married filing jointly to married filing separately after the original due date has passed. Furthermore, if changes affect the amount of tax owed or refunds due, these must be clearly indicated. Completing the M1X involves careful attention to detail, as any discrepancies may lead to delays in processing or potential penalties. Understanding the specific instructions and deadlines associated with the M1X can help ensure a smooth amendment process, allowing individuals to rectify their tax situations in a timely manner.

Form Example

Amended Minnesota Income Tax 2010 |

M1X |

Print or type

Reason for amending

Taxable income

Determining tax

Stock No . 1010090

Your first name and initial |

|

|

Last name |

|

|

Social Security number |

Date of birth (mm/dd/yyyy) |

|||

|

|

|

|

|

|

|||||

If a joint return, spouse’s first name and initial |

Last name |

|

|

Social Security number |

Spouse’s date of birth |

|||||

|

|

|

|

|

|

|

|

|

||

Current home address (street, apartment, route) |

|

|

|

|

|

|

|

For department use only. |

||

|

|

|

|

|

|

|

|

|

|

Do not write in this space. |

|

|

|

|

|

|

|

|

|

Effective interest date: |

|

City |

|

|

State |

Zip code |

|

|

|

|

||

|

|

|

||||||||

Filing status claimed . Note: You cannot change from joint to separate returns after the due date has passed. |

|

|||||||||

On original return: |

Single |

Married filing jointly |

Married filing |

separately |

|

Head of household |

Qualifying widow(er) |

|||

On this return: |

Single |

Married filing jointly |

Married filing |

separately |

|

Head of household |

Qualifying widow(er) |

|||

|

|

|

||||||||

Place an X in the appropriate box to indicate the reason(s) why you are filing this amended return: |

|

|||||||||

Federal audit or adjustment . Enclose |

a complete copy of the IRS adjustment notice and see line 32 instructions . |

|||||||||

Net operating loss carried back from tax year ending |

|

|

|

|

. |

|

||||

Claim due to a pending court case (explain on back page) . |

|

|

|

|

|

|||||

Other (explain on back page) . |

|

|

|

|

|

|

|

|

||

If you show a refund on line 29 or tax due on line 31, you must report an increase or decrease in column B for at least one of the income, tax or credit lines (lines

You will need the instructions for this form and the 2010 Form M1 |

|

|

A. Original amount or |

B. Amount of change |

C. Correct |

|||

instruction booklet. |

|

|

as previously adjusted |

increase or (decrease) |

amount |

|||

1 |

Federal taxable income (see instructions) |

. |

.1. |

|

. . |

|

|

|

|

|

|

|

|||||

2 |

Additions to income (total of lines 2 and 3 of Form M1) . . . . |

. |

2. |

|

. . |

|

|

|

|

|

|

|

|||||

3 |

Add lines 1 and 2 |

|

.3 |

. . . . . . . . . |

|

|||

|

|

|

|

|

|

|

||

4 |

Total subtractions (from line 9 of Form M1) |

. 4. |

. |

. . |

|

|

|

|

5 |

Minnesota taxable income . Subtract line 4 from line 3 . . . . |

. |

5. |

. . |

|

|

|

|

6Tax from the table on pages  . .

. .

7 |

Alternative minimum tax (Schedule M1MT) |

7. |

|

. . . . . . |

|

|

8 |

Add lines 6 and 7 |

.8 |

. . . . . . . . . |

|||

9

line 23 of Schedule M1NR |

. |

9a. . |

. |

b Corrected amount from |

|

|

|

line 24 of Schedule M1NR |

. |

9b. . |

. |

10

from line 27 of Schedule M1NR . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 |

Tax on |

. .11. |

|

. . . |

|

|

12 |

Tax before credits . Add lines 10 and 11 |

. 12. |

. . . . . |

|

|

|

13Marriage credit for joint return when both spouses have earned

income or retirement income (see M1 instructions, page 14) . . . 13

14Credit for taxes paid to another state (Schedule M1CR) . . . . . . .14

15Other nonrefundable credits (Schedule M1C) . . . . . . . . . . . .15. .

16 |

Total credits against tax . Add lines 13 through 15 |

. 16. . |

17 |

Subtract line 16 from line 12 (if result is zero or less, enter 0) |

. 17. |

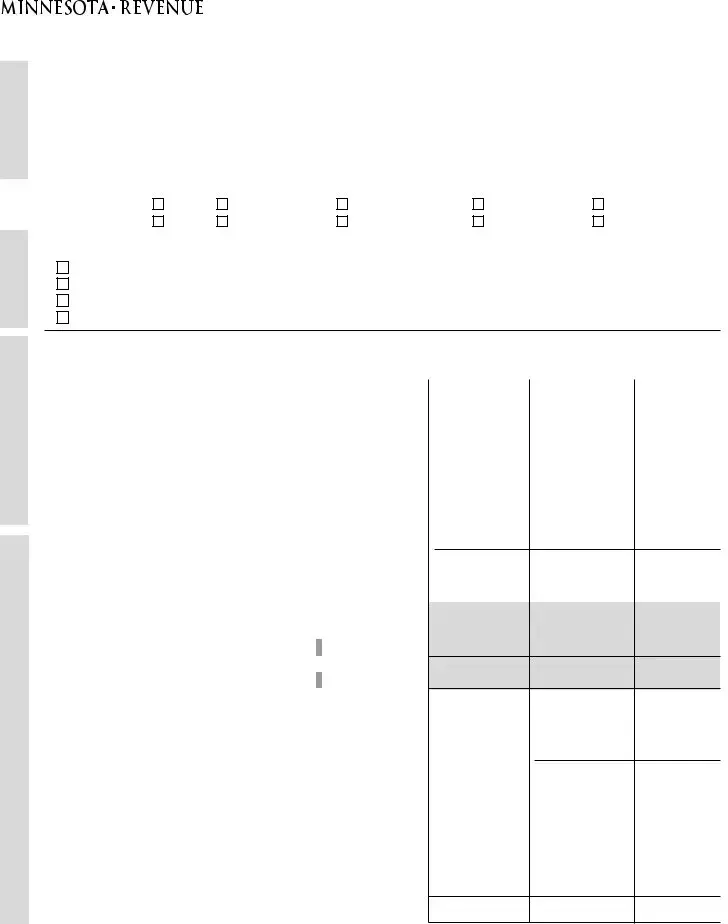

Credits and tax paid

Refund or tax due

Sign here

|

|

|

A. Original amount or |

B. Amount of change |

|

C. Correct |

||||||

|

|

|

as previously adjusted |

increase or (decrease) |

|

amount |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

18 |

Amount from line 17 |

.18. |

. . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

Minnesota income tax withheld (Schedule M1W) |

. 19. |

. |

. |

|

|

|

|

|

|

|

|

20 |

Minnesota estimated tax payments made for 2010 |

. 20. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

21 |

Child and dependent care credit (Schedule M1CD) |

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

22 |

Minnesota working family credit (Schedule M1WFC) |

22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

23 |

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

24 |

Business and investment credits (SCHEDULE M1B) |

. 24. |

. |

. . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

25 |

Amount from line 34 of your original Form M1 (see instructions) |

|

|

|

|

|

. 25 |

|

|

|

|

|

. . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . . . . |

. |

|

|

|

|

|

|||

26 |

Total credits and tax paid . Add lines 19C through 24C and line 25 |

. . . . |

|

. 26. |

. . . . . . . |

|

||||||

27 |

Amount from line 32 of your original Form M1 (see instructions) |

. . . . . . . . . . . . |

. . . . |

. |

.27. |

|

. . . . . . . |

. |

||||

28 |

Subtract line 27 from line 26 (if result is less than zero, enter the negative amount; do not enter 0) |

. |

.28 |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

||||

29 |

REFUND . If line 28 is more than line 18C, subtract line 18C from line 28 and stop here |

. . . . . |

. |

.29. |

. |

. |

|

|

||||

30To have your refund direct deposited, enter the following . Otherwise, you will receive a check .

Account type |

|

|

Routing number |

|

|

Account number (use an account not associated with any foreign bank) |

|||

Checking |

Savings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

31 Tax you owe . If line |

18C is more than line 28, subtract line 28 from line 18C |

||||||||

(if line 28 is a negative amount, see instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . 31. |

. . . . . . |

|

. . . . |

|||||

32If you failed to timely report federal changes or the

|

IRS assessed a penalty, see instructions |

. . . . . . . . . . . . . . |

. . . 32. |

. . . . . . . |

. |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

33 |

Add line 31 and line 32 |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . |

. |

. 33. . |

. . . . . . . . . |

|

||||||||

|

|

|

|||||||||||||

34 |

Interest (see instructions) |

. . . . . . . . . . . . . . . |

. . . . . . . . . . . |

|

. |

. 34. |

. . . . . . . . . . |

||||||||

|

|

|

|

|

Make check out to Minnesota |

|

|

|

|

|

|

||||

35 |

AMOUNT DUE . Add line 33 and line 34 |

. . . . . . . . . . . . . . . |

. . . . . . . . . |

. |

35 |

|

|

|

|||||||

|

|

|

|

|

Revenue and enclose Form M63 |

|

|

|

|

|

|

||||

I declare that this return is correct and complete to the best of my knowledge and belief. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

||||||

Your signature |

|

Spouse’s signature (if filing jointly) |

|

Date |

Daytime phone |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

Paid preparer’s signature |

PTIN or VITA/TCE # |

Date |

Daytime phone |

|

|

|

I authorize the MN Department of |

||||||||

|

|

|

|

|

|

|

|

|

|

|

Revenue to discuss this return with |

||||

|

|

|

|

|

|

|

|

|

|

|

the paid preparer and/or third party . |

||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXPLANATION OF

You must enclose any corrected schedules and, if you filed an amended federal return, a complete copy of Form 1040X Mail to: Minnesota Amended Individual Income Tax, Mail Station 1060, St . Paul, MN

Form M1X Instructions 2010

The 2010 Form M1X can only be used to amend your 2010 Form M1 .

To complete Form M1X, you will need the 2010 Minnesota income tax instruction booklet.

|

Who should file Form M1X? |

|

|

This form should be filed by individuals to |

|

|

||

|

Minnesota individual income tax return. You |

|

|

may not change your filing status from mar- |

|

|

ried filing jointly to married filing separately |

|

|

after the original due date of the return has |

|

|

passed, which is April 18, 2011, for most |

|

|

individuals. |

|

|

Federal changes. If the Internal Revenue |

|

|

Service (IRS) changes or audits your federal |

|

|

income tax return or you amend your federal |

|

|

return and it affects your Minnesota return, |

|

|

you have 180 days to file an amended Min- |

|

|

nesota return. If you are filing Form M1X |

|

|

based on an IRS adjustment, be sure to check |

|

|

the box in the heading and enclose a complete |

|

|

copy of your federal Form 1040X or the cor- |

|

|

rection notice you received from the IRS. |

|

|

If the changes do not affect your Minnesota |

|

|

return, you have 180 days to send a letter of |

|

|

explanation to the department. Send your let- |

|

|

ter and a complete copy of your federal Form |

|

|

1040X or the correction notice you received |

|

|

from the IRS to: Minnesota Revenue, Mail |

|

|

Station 7703, St. Paul, MN |

|

|

If you fail to report the federal changes as |

|

|

required, a 10 percent penalty will be assessed |

|

|

on any additional tax, and the department |

|

|

will have six more years to audit your return. |

|

|

Net operating losses. Use Form M1X for |

|

|

net operating losses, which can be carried |

|

|

forward and back in the same manner as for |

|

|

federal purposes. If you are carrying back a |

|

|

net operating loss, Minnesota generally allows |

|

|

only a carryback to the two taxable years pre- |

|

|

ceding the loss. However, if you are carrying |

|

|

a farm related loss back five years on federal |

|

|

Form 1045 or 1040X, you will carry it back to |

|

|

the same year on Minnesota Form M1X. |

|

|

Filing for another taxpayer |

|

|

If you are filing Form M1X for another |

|

|

taxpayer, enclose Form REV184, Power of |

|

|

Attorney, or a copy of the court appointment |

|

|

authorizing you to represent the taxpayer. |

|

|

If you are claiming a refund on behalf of a |

|

|

deceased person, enclose a copy of the court |

|

|

appointment that authorizes you to represent |

|

|

the deceased person. Also enclose Form M23, |

|

15009010 |

Claim for a Refund Due a Deceased Taxpayer. |

|

Deadline for filing |

||

|

||

. |

To claim a refund, you must file Form M1X |

|

No |

within 3½ years of the original due date for |

|

Stock |

||

|

the year you are amending. Other deadlines may apply if:

• yourfederalreturnhasbeenchangedsince you originally filed, or

• youhavebeenassessedadditionalincome tax by the department within the last year.

If any of the above situations applies to the year being amended and you need clarifica- tion, contact the department.

If you owe additional tax, you must file Form M1X within 3½ years of the due date of your return or the date you filed the return, which- ever is later. If the tax and interest is not fully paid when you file Form M1X, a late payment penalty and additional interest will be assessed on your first bill.

Married filing separate returns

Do not include the name and Social Security number of your spouse if you are married and filing separate returns.

Column A, lines

In most cases, enter the amounts from the appropriate lines of your original 2010 return. However, if your original Form M1 was changed during processing or if you have filed an amended return prior to this one, enter the corrected amounts. If you received a notice of change or an audit report from the department which changed amounts on your original return, use the amounts as shown in that notice or audit report.

Column B, lines

Enter the dollar amount of each change as an increase or decrease for each line you are changing. Show all decreases in parentheses. See the instructions for lines 6 and 10 to determine the amounts to enter in column B for those lines.

If the changes you are making affect the amounts reported on a schedule, you must complete and enclose a corrected schedule.

If you do not enter an amount when there is a change, the processing of your amended return will be delayed. Briefly explain each change in the space on the back of Form M1X and enclose any related schedules or forms.

If you are not making a change for a given line, leave column B blank.

Column C, lines

Add the increase in column B to column A, or subtract the column B decrease from column A. For any item you do not change, enter the column A amount in column C.

Line instructions

Refer to the 2010 Form M1 instructions for de- tails on the types of income included in the total income, any allowable adjustments and how to compute and claim various credits, etc.

Line

Enter the amount from line 1 of your original 2010 Form M1. If your original federal taxable income was previously adjusted by the IRS or the Minnesota Department of Revenue, enter the corrected amount.

Changes to your federal taxable income may also affect child and dependent care, working family and education credits. Your property tax refund return (if filed) may also be af- fected. If it is, complete and file Form M1PRX, Amended Minnesota Property Tax Refund Return.

Line

If you are changing your total subtractions, you must enclose a list of the corrected sub- tractions you reported on lines

Changes to your total subtractions may also affect the alternative minimum tax you may be required to pay.

Line

If your taxable income on line 5C has changed, it will affect your tax from the table. Continue with line 6.

Line

If the taxable income on line 5C has changed, you must look up the corrected tax using the tables in the 2010 instruction booklet. Enter the correct tax amount on line 6C and the dif- ference between lines 6A and 6C on line 6B.

Lines

Changes to your Schedule M1NR will also affect many credits you may claim, such as the child and dependent care, working family and education credits.

Line 10

Enter the difference (increase or decrease) between lines 10A and 10C on line 10B.

Line

If you are changing your marriage credit, complete the worksheet on page 14 of the Form M1 instruction booklet.

Lines 14 and

If you are changing any credits against tax on lines 14 or 15, you must enclose a corrected copy of the appropriate schedule.

Lines

If you are changing any payments or credits on lines 19 through 24, you must enclose a corrected copy of the appropriate schedule.

Line 25

Enter the total of the following tax amounts, whether or not paid:

• amountfromline34ofyouroriginalM1,

• amountfromline31ofapreviouslyfiled Form M1X, and

• additionaltaxdueastheresultofanaudit or notice of change.

Reduce the total by any amounts that were paid for penalty, interest, underpayment of estimated tax or any contributions you made to the Nongame Wildlife Fund.

Line 27

Enter the total of the following refund amounts:

• amount from line 32 of your original Form M1, even if you have not yet received it,

• amountfromline29ofanypreviously filed amended return, and

• refundorreductionintaxfromanaudit adjustment or appeal.

Include any amount that was credited to estimated tax, applied to pay past due taxes, used to pay an outstanding debt to a state or county agency, or donated to the Nongame Wildlife Fund.

Do not include any interest that may have been included in the refunds you received.

Lines 29 and 31

Lines 29 and 31 should reflect the changes to your tax and/or credits as reported on lines

Line 29

This refund cannot be applied to your esti- mated tax account. Skip lines 31 through 35.

If you owe federal or Minnesota taxes, criminal fines or a debt to a state or county agency, district court, qualifying hospital or public library, the department is required to apply your refund to the amount you owe (including penalty and interest on the taxes). Also, if you participate in the Senior Citizens Property Tax Deferral Program, your refund will be applied to your deferred property tax total. Your Social Security number will be used to identify you as the correct debtor.

If your debt is less than your refund, you will receive the difference.

Line

If you want the refund on line 29 to be directly deposited into your checking or sav- ings account, enter the requested informa- tion on line 30.

The routing number must have nine digits.

The account number may contain up to

17 digits (both numbers and letters). If your account number is less than 17 digits, enter the number starting with the first box on the

If the routing or account number is incorrect or is not accepted by your financial institu- tion, your refund will be sent to you in the form of a paper check.

By completing line 30, you are authorizing the department and your financial institu- tion to initiate electronic credit entries, and if necessary, debit entries and adjustments for any credits made in error.

Line 31

If line 28 is a negative amount, treat it as a positive amount and add it to line 18C. Enter the result on line 31. This is the amount you owe, which is due when you file your amended return. You cannot use any funds in your estimated tax account to pay this amount. Continue with line 32.

Line 32

If only one of the penalties below applies, you must multiply line 31 by 10 percent (.10). If both penalties apply, multiply line 31 by 20 percent (.20). Enter the result on line 32.

• TheIRSassessedapenalty for negligence or disregard of rules or regulations, and/

or

• Youfailed to report federal changes to the department within 180 days as re- quired (see page 1 of these instructions).

Line

You must pay interest on any unpaid tax plus penalty from the regular due date until paid in full. Interest rates may change each calen- dar year. For 2011, the rate is 3 percent.

To determine the interest you owe, use the for- mula below with the appropriate interest rate:

Interest = line 33 x number of days past the due date x interest rate ÷ 365

To find

Line

Pay the amount due electronically or by check. Go to www.taxes.state.mn.us or call

Sign your return

If you are married and filing jointly, your spouse must also sign. If you paid someone to prepare your return, that person must also sign and include their preparer identification number.

You may check the box in the signature area to give us your permission to discuss your return with the paid preparer and/or third party.

Checking the box does not give your preparer the authority to sign any tax documents on your behalf or to represent you at any audit or appeals conference. For these types of authorities, you must file a power of attorney or Form REV184 with the department.

Questions or need forms?

Visit our website at www.taxes.state.mn.us to find forms, electronic payment options, etc, or request forms by calling

If you have questions, call

Where to file your Form M1X

Send your completed Form M1X and re- quired enclosures to the address provided at the bottom of the second page of Form M1X.

Use of and required information

Information not required. Although not required on Form M1X, we ask for your daytime phone number, in case we have a question about your return, and the phone number and identification number of the person you paid to prepare your return.

All other information is required. You must provide by Minnesota law (M.S. 289A.08, subd. 11) your Social Security number, date of birth and all other information in order to properly identify you and determine your correct tax liability. If you don’t provide it, the department will return your form to you. This will delay your refund or if you owe tax, your payment will not be processed and you may have to pay a penalty for late payment.

Use of information. All information pro- vided on Form M1X is private under state law. It cannot be given to others without your consent except to agencies authorized by law to receive the information. For a list of au- thorized agencies and for the possible uses of your Social Security number, see page 8 of the M1 instruction booklet.

Form Specifications

| Fact Name | Description |

|---|---|

| Purpose | The Minnesota M1X form is used to amend a previously filed 2010 Minnesota income tax return. |

| Eligibility | Only individuals who filed a 2010 Form M1 can use the M1X to correct their tax return. |

| Filing Deadline | Form M1X must be filed within 3½ years of the original due date to claim a refund or to address additional tax owed. |

| IRS Changes | If the IRS audits or adjusts your federal return, you have 180 days to file the M1X to reflect those changes on your Minnesota return. |

| Governing Law | This form is governed by Minnesota Statutes, Section 289A.08, Subdivision 11. |

Popular PDF Templates

University of Minnesota Urolith - Request for detailed background on animal's previous urolith incidents and dietary habits preceding urolith detection.

To effectively navigate the process of validating your documents, explore the vital components involved in the Notary Acknowledgement requirements by reviewing the necessary form available here.

Mn Tax Forms 2020 - Structured to accommodate both amended returns and no activity returns, making it versatile for different filing situations.